Michael Cheng

Forum Replies Created

-

AuthorPosts

-

-

San Jose is a beautiful city in the middle of Silicon Valley, and home to many attractions such as the Spanish Colonial District and the Tech Museum of Innovation. To help seniors in San Jose find the assisted living community that’s right for their family, we’ve researched and compiled in-depth information about the cost of care, how to pay for care, and important local laws and regulations involving senior care and assisted living.

With an average cost of $4,568 in San Jose, it’s often difficult to find assisted living communities that provide high-quality care at an affordable price. At Caring.com, our mission is to make this process as smooth and painless as possible, and we’ve helped many families along the way.

This guide provides everything you need to quickly compare communities and narrow your search, including 188 unique reviews from residents and our comprehensive database that gives pricing, amenity information, photos and more on the 72 facilities in San Jose.

May 8, 2020 at 6:15 pm #17856 -

As an active Realtor, I’m constantly on the look out for signs of shifts in market conditions. When it comes to the National Association of Realtors (NAR), everything they say should be taken as gospel, NOT!

One of the reasons I became a real estate broker was that I was fed up with the perennial cheerleading from the NAR. Promoting a profession is one thing, willfully disregarding reality to service its member is a sin, making the NAR as culpable as the NRA for performing a disservice. I felt that home buyers and sellers deserved the same rigorous and disciplined analysis of the housing market that is being done by the wealthy bankers on Wall Street. I’ll bet you they don’t follow the NAR’s advice in figuring out how to make billions on the housing market.

So, when the chief economist/propagandist of the NAR, Lawrence Yun, declares there’s NO HOUSING BUBBLE IN SIGHT, I find myself suddenly in a cold sweat. For some reason, his opinion has been a sharp prognosticator of exactly the opposite of what happens. He put out similar articles during the peak of the last housing bubble in 2006-2007, saying essentially the same thing: It’s different this time. Back in 2006-2007, he saw no housing bubble given the boom in household creation and a robust job market, both driven by record monetary liquidity and financing. Today, he’s seeing a similar robust job market as we’ve once again found ourselves flush with loose monetary policies.

Since he made the same calls, I’m looking for signs of a housing bubble popping. So far, I can see that to a certain extent, he may be right. Most of the US has not been caught up in the housing recovery and boom since 2008. Hence, there’s literally no bubble to pop, at least not on the national level. But, in local submarkets, there are signs that home prices are getting unsustainable even with strong employment. What Lawrence Yun twisted around was inferring a low housing sales volume today as a sign that there’s more potential demand. However, sales volume has no bearing on bubble conditions, record high prices and lots of debt are the right signs. To that end, we do see lots of coastal submarkets (Miami, NY, Boston, LA, SF, Seattle) around the US on a tear, with prices for the few homes for sale going way beyond the last housing price peak in 2007. These submarkets exhibit potential bubble conditions.

Yet, just because prices are high doesn’t mean they’ll automatically or immediately come down. In several of these submarkets, SF in particular, price increases are being driven by higher incomes from strong employment, as compared to areas like Miami which are more driven by speculation and foreign investments.

September 10, 2015 at 12:20 am #17432 -

Despite all my criticisms about Zillow’s potential, I’m still pleasantly surprised by occasional savvy moves.

I discussed the horrible decision by MarketLeader to acquire ActiveRain, which was recently spun back out. Then, Trulia bought up MarketLeader to make itself more marketable to Zillow. Trulia paid an obscene sum of $355M for a poor performing business. Now that Zillow swallowed up Trulia and is starting to recognize the dead weight that came along with Trulia, at least it has the clarity to dump MarketLeader while it can still recover some value. Still, $23M for MarketLeader is a pathetic return on $355M in 2013 dollars. Zillow would need to sell for close to $400M just to break even. Oh well, it’s flushing down $4B in value with Trulia anyways, so just another drop in the bucket.

September 3, 2015 at 2:46 pm #17434 -

Regular readers of my blog know I’ve been pounding the table for sustained low mortgage interest rates since 2011. Back then, I saw there was enough global and local headwinds to the economy to tie the Federal Reserve’s hands for years and for a disconnect between the Fed’s funds rate and mortgage interest rates. Earlier this year, I posted a blog to explain my rationale.

Meanwhile, fellow Realtors and some lenders continued to threaten home buyers with higher impending mortgage interest rates, much to the detriment of home buyers. This fear-based message pressures buyers to purchase homes sooner and at higher prices. This also leads fearful buyers to lock themselves into expensive 30-year fixed rate loans where a lower rate 5/1 or 7/1 adjustable rate mortgage (ARM) would be more advantageous.

Today (7-14-15), the biggest mortgage originator in the country, Wells Fargo, concedes they have been wrong about anticipating higher interest rates for years. Wells Fargo finally believes that the Federal Reserve Chair, Janet Yellen, has been crying wolf about higher interest rates (but given the macro-economic conditions, how can you blame her). They now don’t believe there’s a realistic chance of Fed funds rate increases in the near future, and if there were to be increases, they would be gradual and delayed for years. Wells Fargo is betting hundreds of millions to back that belief, buying credit swaps to convert their floating ARM loans to fixed rate loans. In effect, Wells Fargo agrees with my assessment that there’s little likelihood of the ARM loans floating up to the same rates as the fixed rate loans. And, with typical herd mentality, other banks are very likely to follow.

Of course, there’s a certain satisfaction and vindication when the biggest mortgage originator agrees with me and puts real money on the line. This will only be compounded when other banks eventually follow suit. Still, when dealing with the behavior of slow moving institutions, we need to also understand what their behavior actually signals. Just as with media reports on the status of the housing market and mortgage interest rates, we have to separate out their view from the 40,000-foot perspective from what is actually happening on the ground. While I haven’t changed my assessment of the direction of mortgage interest rates yet, I certainly won’t be waiting until Wells Fargo reverses course and repositions themselves for a higher mortgage interest rate environment.

July 15, 2015 at 12:00 pm #17413 -

I recently came across an opinion on the investing site, Seeking Alpha, that touted Zillow stock as undervalued and it got me thinking.

The writer believes that Zillow’s recent acquisition of Trulia puts it in position to capture the majority of online advertising growth for real estate. Since real estate advertising is a huge market, Zillow has potential for huge growth. While I do not dispute that the potential is there, I doubt that Zillow will execute to deliver those results.

For context, the Trulia acquisition basically made Zillow the only real player in the real estate online advertising industry. (Specifically, I consider what Zillow offers Realtors is advertising and not actual marketing.) Trulia had itself just acquired MarketLeader, which in turn had acquired ActiveRain and RealEstate.com. (See my post here.) In effect, buying Zillow stock meant you were betting on the entire industry, just like buying Tesla stock would be for the electric car industry. For some investors, that convenience justified a premium for the leading company, just like Cisco during the late 90s Internet boom and Apple with the current niche industries it created.

So, just like Cisco’s stock outperformed in 1999 in anticipation of its industry dominance, the reality often fails to live up to the hope. That is what concerns me about Zillow. When Zillow acquired Trulia for $3.5B in stock, it joined two powerhouse companies, each with its own successful culture and business model. Trulia in particular had built a fiercely loyal and protective following amongst the Realtor community with a system that rewarded valued contributions with customer visibility. It was a beautiful crowd-sourcing content model that allowed Trulia to grow quickly while building the businesses of the supporting Realtors. On the other hand, Zillow had benefited from a first-mover advantage and did not need the support of Realtors to generate clicks. Instead, Zillow was more focused on monetizing those clicks than continuing to build relationships with the Realtor community.

With such differing approaches, there were two options for the Zillow-Trulia acquisition: dump one and lump all the remaining eyeballs together or keep both and continue to grow with different audiences. At the Zillow leadership, the first and more conventional option was selected. As a result, all the dedicated Realtors, who had spent countless hours crafting a brand for themselves with consumer-friendly blogs and earnestly answering millions of consumer questions, found themselves unceremoniously dumped to the side, with blogs and answers deleted without notice. These Realtors were immediately bombarded by the Zillow sales force to sign one of many pricey advertising packages to retain any semblance of relevance. Of course, none of these packages offered any brand or marketing value. At the same time, consumers were left in a lurch as the seasoned and detailed feedback from actual Realtors were replaced by pointless and irrelevant postings by Zillow staffers.

To me, such a slash and burn approach seemed more like 2 + 2 = 2. Hence, Zillow’s stock has been on a straight downward trajectory since the bump from the Trulia acquisition announcement. While Zillow might continue to grow from 3 to 4 as the defacto industry player, its long-term profitability is still in doubt. Whether Zillow admits it or not, it has had the good fortune of operating during one of the best housing market environments that most people can recall, even including the last boom from just 8 years ago. Yet, Zillow has consistently lost money for the past 10 quarters, only surviving on continued sales of its high priced stock. Perhaps the massive consolidation of the real estate marketing industry is just a high price to pay for future industry dominance, but I just do not see how Zillow can ever grow into its sky-high valuations. (Without going too deep into stock analysis, it just does not seem sustainable for Zillow to increase selling expenses by 237% when revenues only went up by 179% in two years.)

Real estate has always been about relationships. For a company like Zillow that is willing to sever millions of valued relationships with their Realtor customer base, that incongruence will not end well with the consumers. Even now, with Internet marketing so prominent, most successful Realtors I know still base most of their business on old-fashioned referrals and introductions. Perhaps Zillow can still grow massively with those who need to advertise to grow their business, but with the commoditization of websites, successful Realtors will find cheaper alternatives. That does not even consider the scenario where the real estate market cools and the once aggressively advertising Realtors find that results from Zillow were not as good as they hoped and cut back on those spending sharply.

For me, I would prefer to sit out of Zillow.

Update (7-9-15): Apparently, the situation at Zillow is deteriorating even faster than I thought. Just a month after my posting, Zillow’s CFO jumped ship. If anybody knows the extent of the financial disaster at Zillow, it would have to be the CFO. Investors are heading for the door too. If Zillow can’t grow in the midst of the strongest housing market in decades, it’s as good a short-sale candidate as any.

Update (8-4-15): Less than 45 days from my initial posting, Zillow stock is down over 20% and short sellers can smell the chum in the water. Sell-side analysts are piling on top of each other to post low price targets of $60 or even $40 a share for Zillow in the next 12 months. Given the rapid deterioration in the growth prospects of the business and the generally disgruntled customer base of real estate agents, the downside trajectory suggests a price target of $25-40 in the next year.

With the earnings release today, the headline numbers looked great and Zillow stock shot up back to $80/share with a massive short squeeze. The company shifted its growth focus on milking more out of each agent and actually decreased the number of agent customers. While this may increase the net profitability, growth will be limited. And with any slight downturn, the smaller pool of agents will increase the risk to revenues. Ultimately, it pains me to see fellow agents forking over $2M a day to Zillow, which took our data from our MLS to steal our customer leads and then sells those leads back to us.

Update (8-5-15): Looks like Wall Street analysts and investors agree with my assessment about the risks to growth for Zillow if they only focus on squeezing more out of a smaller pool of “crazy” agents. Plus, what was the point of paying so much for Trulia if Zillow only wanted to keep a handful of profitable agents? After briefly breaching $80/share at the open, it’s already down 10% in the same day. Look out below.

June 9, 2015 at 1:16 am #17386 -

Sometimes, I’m at an absolute loss as to the reason (besides a paycheck) why somebody would write an article about which they know nothing about and contributes nothing.

Here’s a prime example from Business Insider:

http://www.businessinsider.com/silicon-valley-unaffordable-even-for-engineers-2015-5

The article refers to some real estate search datasets from Redfin. The author makes a huge stretch of the imagination and suggests that home seekers must be searching outside the Silicon Valley as homes here are no longer affordable. Though she was born in Southern California, she’s now a New Yorker and clearly betrays her provincialism with her outsider’s perspective of real estate and the Silicon Valley. She even uses a photo of San Francisco and proceeds to use Bay Area and Silicon Valley interchangeably.

As with my prior post about the same silly conclusion from the CAR president, I need to re-iterate the reality that high real estate prices are not causing young home buyers to search outside the area. The causal relationship is reversed. The strong desire of young home buyers for awesome Bay Area living near top employers is driving up the local real estate prices.

When the Redfin datasets show that more home seekers are looking outside the Silicon Valley, the reasons are patently obvious to anybody who is active in Silicon Valley real estate. Searches for Sacramento are up as investors who are priced out of the Bay Area look for the next best alternative. Interest in Seattle is increasing with Amazon and Microsoft poaching Silicon Valley’s unmatched tech talent.

At the same time, Southern California (SoCal) searches are down, debunking the article’s thesis. Anybody who lives in Northern California (NorCal) and has seen the once thick snowpacks on the mountains go bare can easily understand why that’s the case. And with the infamous SoCal/LA traffic, there really shouldn’t be any surprise.

As for minor uptick in searches in other areas, the reason is even simpler–Redfin has recently expanded the number of cities it covers outside the Bay Area.

While there’s some validity to her suggestion that software engineer salaries aren’t keeping pace with price appreciations in the Silicon Valley, the reality is that local buyers don’t entirely depend on their salary to save up for their down payments. Huge numbers of software engineers have cashed out significant sums from stock options and awards, which have been rapidly increasing and driving up the local home prices.

To be successful in the San Jose Bay Area and Silicon Valley real estate, buyers need to be armed with sophisticated advice from seasoned professionals. Drivel off the internet needs to be read with caution.

May 29, 2015 at 2:18 am #17304 -

While I’m a Realtor broker in the State of California, I’ve never been a fan of the California Association of Realtors (CAR), an industry organization that I’m forced to join in order to have access to basic professional information about properties.

Most of the time, the CAR tries to leverage its member-backed resources to promote policies that support the profession. Unfortunately for consumers, this usually means a jealous guarding of the status quo, where a lack of transparency and clarity is used to protect the profession. Hence the absurd requirement to be a member of the CAR just to access property databases. (In reality, the databases are just the starting point.) However, I’ve come to accept and even embrace this conservative aspect of the profession, which is powerfully resistant to change and only adapts new technology on a glacial time frame.

Still, I’m occasionally surprised by the ridiculous statements that escapes from this turgid organization. This pronouncement from the CEO of the CAR is a perfect example:

In this article, CAR CEO Joel Singer is quoted to have made a rather non-sensical logical leap that the current high home prices in California would force the Millennial generation of home buyers to buy homes out of state.

My only guess at how such a reasoning came about is to go back to basic macro-economics. Somehow CEO Joel Singer thinks that real estate is just like any other fungible commodity, one home is exactly the same as another, regardless of location. Hence, higher priced home in California would lead price-sensitive home buyers to go outside the state.

While that is in itself a reasonable argument, it violates the basic tautology of real estate – location, location, location.

A Millennial homebuyer in the Bay Area would be better off paying $400-500K for a nice 1 bedroom condo if he makes $150-200K a year than go out of state, perhaps into the desert wilderness of Nevada to make $35-50K a year and pay $100K for a similar condo. Sure the income to home price ratios are similar, but that extra $100K a year in income can sure buy a lot of other benefits. It’s simply not feasible to compare the two locations as both being viable to the Millennial homebuyer. The $150K/year job is simply not available out in the desert. Even with a lower standard of living, the fewer dollars still doesn’t go as far.

Frankly, I sometimes wish the CAR leadership would focus more on ways to make the real estate profession more efficient instead of spouting off nonsense.

May 5, 2015 at 1:21 am #17261 -

Three years after our post on buying a home in Silicon Valley, the market has sharply changed. From the bidding behavior we’ve observed, it’s tempting to say that buyers should throw the old playbook out the window. But, before they do, they need to find a new set of rules to succeed in this market. Let’s discuss them here.

While many of the same drivers in the Bay Area housing market remain the same, additional factors contribute to continued strengthening in the Silicon Valley home prices, driving them far ahead of the slowly recovering or stagnant housing market for the rest of the country. Based on our current experiences with homebuyers and investors, the competitive landscape is now tougher than ever before. Already high Bay Area home prices are actually accelerating in their rate of appreciation as low inventory creates its own feedback cycle.

As discussed in our post on the direction of mortgage interest rates, the interest rate environment is supportive of Bay Area home prices going upwards for some time. However, that in itself doesn’t quite capture the local real estate market. What is happening now with Silicon Valley real estate is being driven by the continued participation of cash buyers, who are not interest rate sensitive. Back in 2012, the cash buyers were mostly investors. The cash buyers today are homebuyers who have managed to either save up or borrow enough cash to buy a home without the hurdle of a conventional mortgage.

Traditionally, cash buyers are the lowest bidding buyers as they offer the best terms for the Sellers. That was the main reason cash investors were able to get some really good deals back in the 2009-2011 housing correction, when a shell-shocked financial system made conventional mortgages very tough to get. However, the situation is very different for cash buyers today. With so many other sources of funds available to cash homebuyers, including uncollateralized loans, it actually makes some sense for these cash buyers to also be the highest bidders.

This counterintuitive behavior by cash buyers puts conventional home buyers with mortgages at a devastating disadvantage, as described in detail here. In a competitive bidding situation, cash buyers can easily waive all contingencies as they are not beholden to a lender’s underwriting requirements. The biggest hurdle is the appraisal. With Silicon Valley home prices going up so fast, getting a home appraised for the contract price is quite challenging. Appraisers are very poor judges of market value and only use antiquated techniques and old data to justify a home’s value for the lender. After all, that’s why few people ever consider the appraised value to be the actual market price.

Usually, well financed home buyers could put down additional funds to cover appraisal shortfall to compensate. But, with conventional homebuyers planning to put down 10-20%, cash buyers can easily dominate by bidding 10-20% above recent market comps, ensuring the appraisal shortfall is too much to cover for financed homebuyers.

Similarly, a financed homebuyer needs a home to be in satisfactory condition from the appraisal report to even get a loan. Otherwise, if a home has an issue, something as simple as missing a stove, that could prevent a financed homebuyer from getting approved. It’s that silly. Yet, it’s situations like this which prevent the financed homebuyers and the sellers from getting a high level of confidence about a deal closing.

Finally, a cash buyer is able to move much faster. Rather than at least 3 weeks or more for a financed homebuyer to get a loan through, mostly taken up by the appraisal process, a cash buyer can easily close in days or a week. This shortens the amount of time the seller needs to worry about the deal closing. And, it’s about to get worse for the financed homebuyer as well-meaning financial regulations are being enacted that will extend the financing time by at least 3 more business days, which can easily end up being an extra week.

So, after all this, the conclusion is inevitable, if difficult to swallow — homebuyers have the best chance of success if they can buy with all cash.

But, let’s say this cash option is not possible. There are plenty of other ways to successfully win a home in Silicon Valley besides direct competition.

Market strategy #1: One of the best strategies for financed home buyers today is to go with a pre-construction home project. Buying a home directly from a builder offers both additional appreciation opportunities and a level playing field against cash buyers, as builders will often finance the homes they sell. Of course, with the number of financed buyers far outnumbering the available homes that will be built, the key is to gain access to the right home construction projects far in advance, often before there is even a sales trailer. For clients who have done so with us, their results have been spectacular. Typically, they are gaining 20-30% in price appreciation within the first year.

Market strategy #2: A re-emerging trend in response to the cash buyers has been the prevalence of off-market deals. While many wonder at the rationale behind a Seller willing to do an off-market deal, the reality is that there are many valid reasons where an off-market deal actually benefits the Seller even in a seller’s market. Actually, the deals are not purely off-market, just off-MLS. Of course, the traditional MLS companies don’t like deals that take place off the MLS and will use scare tactics to deter buyers. The truth is that most real estate transactions take place off-MLS, including the new homes mentioned above. So, while MLS listings provides a valuable service to buyers and sellers, it is still a small slice of the available inventory. This is where working with agents who can go beyond the MLS will really give you an edge.

Market strategy #3: When the housing market is hot and it is difficult to win the home you want, it is often a better choice to build your own home. You have the benefit of fully customizing everything to your liking, and in today’s market, it can be actually less expensive than buying an existing home. Of course, there are downsides. Building from the ground up typically takes 12-18 months, and the amount of time and attention needed from the homebuyer is significant. Still, this is a very viable option and is actually far more common than most homebuyers think. For all the new homes built every year, 50% are built by small home builders who may only build 1-6 homes a year. Today, with low-cost construction financing becoming much more accessible to homebuyers, this is the best time to build your own in the past 10 years.

April 4, 2015 at 8:43 am #17106 -

Are Mortgage Rates Going Up in 2015?

Regarding the direction of mortgage interest rates for 2015 and beyond, there are two polarized opinions. On the popular side are many Realtors, loan officers, and economists who keep buying into the Federal Reserve’s meeting statements about raising interest rates this year. On the other are finance professionals and savvy homebuyers who are actually betting on flat to lower interest rates. So, why the difference in opinion and who might be right?

The mortgage interest rate pundits

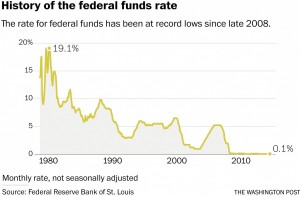

For the rate increase camp, let’s examine the source of their insistence on higher rates, the US Federal Reserve Bank, which ostensibly “sets” interest rates. Here’s a nice historical chart by the Washington Post of the federal funds rate, the rate charged by the Federal Reserve Bank to member banks. This rate sets the floor for the cost of money in the US and underlies an enormous range of bank originated loan products, including home mortgages. So, the lower the federal funds rate, the lower the mortgage rate banks can charge and still make a very tidy profit.

As we can see by the chart, the federal funds rate had been on a long decline for 30 years before flatlining in late 2008 when the Federal Reserve hit the panic button in the midst of the Great Recession. For better or worse, the near zero federal funds rate meant a huge flow of cash poured into the surviving banks, which were simultaneously chastened and told to lend the cash out only to borrowers who met very high underwriting standards–a tough spot to be. As a result, banks sat on enormous balance sheets and had to compete hard for qualified borrowers with ever lower mortgage rates, which we witnessed from 2009 to today.

Of course, the Federal Reserve didn’t idly settle on its accommodative policy of near zero federal funds rate. After just two quarters of near zero federal funds rate, the Federal Reserve started to suggest at its meetings in 2009 that it planned to raise the federal funds rate. This led to possibly the greatest game of crying wolf in history. Every six weeks, the Federal Reserves would try to jawbone the market into pricing in higher interest rates, by choosing cryptic wordings in its statements that suggested more or less “tightening”. Dozens and dozens of meetings took place from 2009 to today and there’s still no increase in the federal funds rate. The increase always seems to tantalize just over the horizon — maybe this summer, or fall, or winter… And still, so many Realtors, lenders, and economists mindlessly buy into the Federal Reserve’s statements, as if they still mean something more than economic propaganda.

Such mindlessness serves no one any good, especially not the clients of these Realtors and lenders. Yet, the irony is that it’s actually self-defeating for real estate agents and lenders to suggest higher rates are coming soon, in an attempt to stoke buyers into a deal today. Their reasoning goes as such — in a theoretical economic model, if mortgage rates do go up, then housing affordability goes down (the reason they say you should buy now). But, if fewer people can afford a home, demand for housing falls and prices will follow. It’s been a generation since this happened, but it was only in the late 1970s and it was real. Anybody who had the cash to buy then are probably looking at a 10-20x return on their home. Today, there are other factors in play that obfuscate this relationship, but they don’t eliminate it.

A revealing look at the situation

So, if we step back from the rote repetition about the Federal Reserve statements, let’s see why rates are more likely to stay flat or actually head lower. As is the nature of a true market, the odd bedfellows in this camp comprise the most sophisticated financial professionals on Wall Street and the average joe homebuyer. What do they know that we should be thinking about?

For some answers, we have to go back to the fundamentals. Market interest rates reflect demand for money in a market economy, and there hasn’t been a whole lot of demand lately. While economic output in the United States seems to be improving with positive Gross Domestic Product growth, most people intuitively feel as if there has been little change in the past few decades. As pointed out by the Tea Party, the Occupiers, and others, there has been a widening gulf of inequality in this country, largely being engineered by government policies and special interest objectives.

Everyone just outside of the top 5% of income has seen his relative earning power compared to the costs of goods and services decline for the past 30 years The Federal Reserve has been participating in one of the largest peacetime wealth transfers in history. By creating top-down monetary stimulus programs (obscurely named “quantitative easing”) to purchase US Treasuries and mortgage back securities from Freddie Mac and Fannie Mae, the Federal Reserve has pushed enormous piles of cash into banks and major institutional investment funds. The belief was that the cash would trickle down into the economy. However, they aren’t investing the cash as they don’t see enough opportunities to place their sudden windfall. So, money is not flowing through the economy to generate economic activity and thus demand for money.

In a perverse way, this creates a negative feedback loop for the average American consumer, with a giant sucking sound from their modest net worth. With few good investment opportunities, bank and institutional investors continue to pile into low yielding bonds, leading to abnormally low interest rates and spend their time and cash churning out more mortgages, which are sold back to Freddie Mac and Fannie Mae, who then sold back to the Federal Reserve until the end of the quantitative easing programs.

At the same time, companies are not investing much as they’re also trapped in the viscous cycle (except for the high flying tech companies like Apple, Google, or LinkedIn). With the wealth transfer to the rich, the lower 95% of income earners make less money to buy the goods to needed to justify further investments. So, most just pile their trillions of dollars in retained earnings into financial engineering like stock buybacks to drive higher share prices and dividends for the investors, who also happen to be the top 5%.

Therefore, rather than plowing money through the economy to drive growth, the Federal Reserve, banks, and major corporations are all just holding onto ever larger proportions of national wealth in their hands, now well into multiple trillions of dollars. They play a game of musical chairs, shuffling money back and forth with the Federal Reserve printing money to pay for interest and transaction costs. This leads to insufficient investment in both people and productivity, which has led to a declining middle and lower class. When the vast majority of the population has less purchasing power and willingness to spend, there’s less demand for money, perpetuating the cycle.

Other countries with less dynamic economies have already withered under the weight of this vicious cycle and have had to deploy ever more unconventional monetary tools to stave off dreaded deflation. Indeed, they’ve taken lessons from our Federal Reserve and Treasury Secretary and gone further. The European Central Bank has mimicked us (after loudly criticizing our moves in 2009) with their own $1.2 trillion dollar quantitative easing program for 2015. Instead of merely stimulating with easy money policies, they are actually penalizing the money hoarders they created by charging negative interest rates.

Unfortunately, such extreme measures require a robust rebound in economic productivity to unwind, which we are no where near. So, it is now more likely that other countries will have to continue escalating their tactics with ever more risky and exotic policies, which is more likely to result in negative interest rates. Still, unless policies change to stop this giant transfer of wealth to the already wealthy, the vicious cycle won’t stop and demand for money will continue to decline, making ever more crazy situations become reality, like zero percent mortgage rates.

So, what does this mean?

By textbook definitions, impending deflation should cause asset prices like housing to fall, especially if zero percent interest rates aren’t sufficient to generate inflation. But, the relationship is more complex. As institutional investors fail to find better investment opportunities, having already driven up the global stock markets to record highs, hard assets like real estate become more attractive. They’re now sweeping up all the top property assets around the world, paying ever more eye-popping prices as they convert their cash windfall into tangible assets. For example, the landmark Waldorf Astoria in New York City just sold for a record $1.95 billion to a Chinese insurance company, who apparently had nowhere better to place their cash. After holding on to this iconic property for almost 65 years, Hilton Hotels decided that was a deal they couldn’t refuse. Of course, Hilton immediately redeployed the cash into other assets to avoid income taxes.

On a more practical note, this situation also means the average consumer should also be doing the same with their earnings and convert their cash into hard assets like housing. Otherwise, the investment activities of the wealthy and other concentrated wealth will price properties out of reach of average consumers, just like in China.

Yet, as with any financial advice or recommendation, there is an expiration date and one that is being actively monitored at Archers Homes. The market is constantly moving and consumers who can act with the same market insights as hedge fund managers will see similar benefits. For now, we see mortgage interest rates remain steady if not lower for the remainder of 2015. Taking the simplified economic relationship described above, this situation implies that housing prices should continue going up as affordability increases.

Final note

Of course, there are many other factors at play, including stricter underwriting standards, inflows of foreign capital, increases in employment and household income, shift in weather patterns, etc., that also impact housing prices. But those need to be analyzed on a case-by-case basis and will be further discussed in future postings.

March 30, 2015 at 11:41 pm #17063 -

Here in the Bay Area, there’s no mistaking that the real estate market is on a sharp rebound. Thousands of buyers and investors have taken notice. Since plenty of stories abound about investors making big money on real estate in the past few years, many first-time investors are diving in. As I specialize in working with property investors, here are the top five mistakes that I see investors make:

1. Buying properties in unfamiliar markets

This is a very common mistake, one that speaks to the low-hanging fruit nature of novice investing in any asset class. If you don’t know where to start, you tend to go with whatever your neighbor or somebody on TV tells you. It’s not a good or bad idea — it’s just higher risk when you can least afford it. The headlines are always attractive, but if you don’t know the market, you don’t know if you’re getting one of those advertised deals. You can be in the exact same market as the winners and end up in a dump that happens to be on the wrong side of the street.

2. Underestimating expenses

Real estate is a complex asset class. That complexity offers opportunities for the experienced and pitfalls for the novice. As an investment category, there are a large number of possible expenses that a first-time investor would not be aware of or know how to properly calculate. Just on taxes alone, there are transfer, supplemental, and property taxes. On the often touted foreclosure deals, there could be hidden liens, litigation, or undisclosed structural issues. Usually, these unknown expenses are learned through expensive trial-and-error, the same process that real estate brokers and their salespersons go through on a daily basis.

3. Accepting negative cash flow

Less common than in the boom days, first-time investors still think that investing in pricey California means they have to accept no cash flow and even put money in to support the investment. These investors hope that appreciation returns will offset the negative cash flow and bail out the investment in the long run. Often, this means they’re investing in “good” school districts and in nice single family homes. While it is possible to make money in the long run with this approach, the overall return would be less than that of a positive cash flowing property, which would also appreciate.

4. Underestimating the competition

Unlike competing with other home buyers, competing with property investors is a whole new game. Many property investors do it professionally and they know all the tricks of the trade. They’re well prepared with their finances and have a experienced team of lenders, lawyers, and contractors. So, just because a property is a distressed short sale or bank-owned unit, it doesn’t mean you can instantly capture the discount by bidding at the below-market list price. Winning deals, especially in the currently hot real estate environment, takes effort and a bit of old fashioned cunning.

5. Going without an Investment Realtor

This is probably the most serious mistake. Yes, it seems elementary to just buy and rent a property, but that’s the 30,000 foot perspective. Success in property investing depends on proper execution on every step of the process — understanding market conditions, finding the right deals, winning those deals, making the profitable improvements, getting the right tenants, and managing the property. If you go on your own, there are dozens of ways to make a costly mis-step. Even if you work with a regular buyer agent, you’re still left with figuring out how to deal with the property after you’ve purchased it. Regular buyer agents just want to sell you the property and have no accountability for delivering the rental returns. It’s very easy to sit six months or more on a vacant property without the right management. Flipping property is a whole other story, with even more challenges.

So if you’re considering becoming a property investor, make sure you’re educated on these issues or have the right guidance along the way. If you need help in the Bay Area or have any questions, drop me a line (650-275-2594) or send me an email (michael@archershomes.com)

January 10, 2013 at 3:34 am #2514 -

For over a year, I wondered about the construction underway on a patch of land next to Frank Santana Park in San Jose. Tucked inconspicuously between Stevens Creek Blvd and 280, I passed this site regularly on the way to my office behind Santana Row.

Late in 2012, the mystery was finally revealed. It’s KB Home’s brand new community of townhome-style condos called Vicino. Vicino offers an interesting twist to urban living. On one side of the narrow lot is an established community of newer single family homes with great curb appeal and across the street, it’s a row of older ranch homes. On the other side you have the 280 sound wall and a San Jose City fire station. Finally, at the backside of the lot, you’re bordering Frank Santana Park. So, you get much of the feel of the single family living experience with the neighborhood feel and a generous city park combined with modern styling and the low maintenance of condo ownership.

At the far end of the lot, you are within walking distance to Santana Row, one of the most popular destinations for all of San Jose. This proximity is perfect for urbanites, since all the shops, restaurants and bars are just minutes away from your doorsteps, which is especially great for late evening outings.

The floor plans are typical of KB Home’s pragmatic style. Most are 3 story townhomes with side-by-side 2 car garages. Amazingly, there appear to be four units planned which are 2 story townhomes, a very rare find for new homes in the south bay. The 2 story floor plan offers a very desirable layout with the main living area right on the first floor and the bedrooms on the second floor. Otherwise, the floor plans range from 1459 to 1812 sqft and base prices start from the high $600Ks to the low $700Ks. The HOA fees are also quite reasonable.

At the moment, there are no model homes yet and the sales office is in a temporary shared space with Intero in Santana row. Priority reservations for well qualified buyers are being offered with each release. Few, if any, units will be available to the general public. If you’d like to find out more about exclusive deals available or interested in getting a priority reservation in this community, call Michael (650-275-2594) or email (michael@archershomes.com).

September 4, 2012 at 7:23 pm #2180 -

A year after Pulte Homes broke ground on the barren patch of land on the corner of Jackson and Berryessa, Taylor Morrison joined in early 2012 with its own offering of new townhomes called Cherry Blossom. Sharing very similar floorplans with Pulte’s Pepper Lane, the Taylor Morrison townhomes at Cherry Blossom are a bit smaller but differentiate themselves with a lower price point per sqft.

But, lower price doesn’t automatically mean better value. Here are some of the differences between Cherry Blossom and Pepper Lane. Cherry Blossom is a smaller community, comprising of 53 homes, which is just a fraction of the size of Pepper Lane. This means there’s a smaller common community area available. Cherry Blossom is also closer to Berryessa Road, placed right behind the sound wall which divides the townhouse from the future shopping strip facing Berryessa. And, most of the homes at Cherry Blossom have tandem 2 car garages, unlike the side-by-side garages at Pepper Lane.

Here’s how Cherry Blossom comes ahead of Pepper Lane. The fit and finish are similar since they use many of the same contractors as Pulte Homes. So you’re getting a comparable home at a lower price. Plus, Cherry Blossom has better standard features. Many of the units include granite countertops, hardwood and tile flooring, and upgraded cabinetry as standard.So, the townhomes at Cherry Blossom represent solid values given their desirable location. Since they are located directly next to higher-priced Pepper Lane, they will definitely benefit from long-term appreciation, especially as the BART station at Berryessa gets up and running in the next few years.

As inventories around the south bay have been very tight, these townhomes offer an excellent opportunity for first-time home buyers to get a deal as we enter the fall season.

Since the community is just being launched, there are some special deals available to the first few buyers. If you’d like to find out more about the included standard options or are interested in visiting this community, feel free to call or email me.

September 4, 2012 at 7:17 pm #2176 -

Across from the Celadon townhome community in Berryessa, another abandoned Pinn Brothers Construction project is being revived, this time by Trumark. Formerly known as Grandview Terrace, the development stalled in 2008 with the housing downtown. Only 11 of 45 units were sold, while the rest of the community was left vacant, with units in various stages of completion.

For most people passing by, it's hard to tell the community was incomplete for the past 4 years. By contrast, it looked far better than its sister community across North Capitol Avenue, which was little more than a few buildings surrounded by empty fields until Warmington Homes came in October 2011 to finish building Celadon.

For most people passing by, it's hard to tell the community was incomplete for the past 4 years. By contrast, it looked far better than its sister community across North Capitol Avenue, which was little more than a few buildings surrounded by empty fields until Warmington Homes came in October 2011 to finish building Celadon.As of March 2012, this community was acquired and rebranded Capitol Station by Trumark. Construction is being finished off quickly as most units were close to complete. The first units of the 34-unit collection should be ready for sale by June, just in time after Memorial Day.

Five floor plans range from two to four bedrooms and 1316 to 1809 square feet, nearly identical

to Celadon's across the street. With the supply of new homes in Silicon Valley still very tight, these new townhomes will be a welcome addition. Pricing start in the very affordable $400K-500K range.

Stay tuned for further updates or contact me for the latestreleases.

Update 6-19-12: Most of the units have sold out. About a handful remain in the current phase. Call me for the latest availability of the last phase.

May 27, 2012 at 2:16 am #1967 -

Just a month after I posted the first half of this blog, the real estate market turned on a dime. On a national level, sales activity has picked up sharply while prices remain stagnant. But, locally in the Bay Area, housing suddenly has turned red hot. Good properties no longer lingered on the market for weeks or months. By February, they were snapped up with stunning ferocity, often with dozens of offers far above asking on the first weekend.

Just a month after I posted the first half of this blog, the real estate market turned on a dime. On a national level, sales activity has picked up sharply while prices remain stagnant. But, locally in the Bay Area, housing suddenly has turned red hot. Good properties no longer lingered on the market for weeks or months. By February, they were snapped up with stunning ferocity, often with dozens of offers far above asking on the first weekend.In the midst of all this, I found myself as thunderstruck as most other local agents by the strength of housing. There was no particular news to drive the shift, as unemployment remained high and the government wasn't providing any more incentives. But, the reality we saw was fierce bidding wars, going in far above asking and often losing out to an all-cash buyer who didn't need to worry about appraisals.

What could explain this sudden stampede? As with any shifts in herd-mentality, the underlying cause was years in the making.

As discussed in the first half of my blog, when an asset class collapses under the weight of overleveraging, fear pervades throughout the investor pool. So, when housing collapsed in 2007 and dragged down the economy and the stock market, investors sought relative safety in cash and government backed debt. This led to record low interest rates for debt instruments, which was compounded by the ineffective efforts of central banks around the world to use monetary policy to fight the inevitable deleveraging. (China and the developing world weren't as heavily leveraged, since they didn't have that privilege, so their economies responded well to monetary stimulus.)

Of course, when one asset category shoots sky-high, investors immediately looked for ways to offset the perceived increase in risk. (In hindsight, they were correct to be fearful as the continuing Euro sovereign debt-crisis illustrates.) So, this fear trade led to all sorts of distortions, principly in commodities as oil, gold, silver, etc. all shot up to record highs. Even now, they're not far off those records. Then, once those got very high priced, investors rotated back to depressed equities on the stock market. Now, we are within shouting distance of the bubble peaks, at least on the broad market basis.

Then, with all these investment categories at or near record highs, the fearful investor has few places to turn. But, thankfully, housing had been soundly beaten down and until February this year, the pundits were still brow-beating it. So, prices remained low while rents climbed from a still growing population.

Perhaps it just required the seasonal pickup in homebuyer activity to drive the already eager investor buyers into a frenzy. In any case, when buyers had to line up for their turn at open houses, the market signal was unmistakeable. With bids climbing, cash-heavy investors were still in the best position to win deals. They've done their analysis (or worked with an investment Realtor) and know how much room is left in deals, allowing them to out-bid homebuyers while still making a good return. With interest rates still being held to record lows, even a 4-5% ROI (30-40% lower than 2011) is attractive.

Meanwhile, credit remains relatively tight so many homebuyers find themselves in the rather unsavory position of having to bid obscene premiums above asking prices to be competitive against investors on prime properties. Investors for their part have very good credit ratings and can get leveraged returns in the double-digits, justifying ever higher offers.

When will this end? It's hard to say only because it's so early in the cycle for housing. We're still far below the price records of 2007. Many Bay Area condo communities are still 60% below the peaks, making the recent 10-20% price spikes seem trivial. Plus, much of the price appreciation is being driven by cash or cash-heavy buyers who aren't going to be affected even if interest rates rise. And, with rental returns still very solid, we may be in the middle of a steep 2-3 year recovery cycle. While occasional speed-bumps on the path to recovery are unavoidable, the savvy investor or buyer will lock up good deals whenever possible as the housing market makes it way back toward the peaks.

May 7, 2012 at 2:33 am #1958

-

Share this:

- Share on Facebook (Opens in new window) Facebook

- Share on LinkedIn (Opens in new window) LinkedIn

- Share on X (Opens in new window) X

- Share on Pinterest (Opens in new window) Pinterest

- Share on Reddit (Opens in new window) Reddit

- Email a link to a friend (Opens in new window) Email

- Share on Tumblr (Opens in new window) Tumblr

- Print (Opens in new window) Print

- Share on Pocket (Opens in new window) Pocket